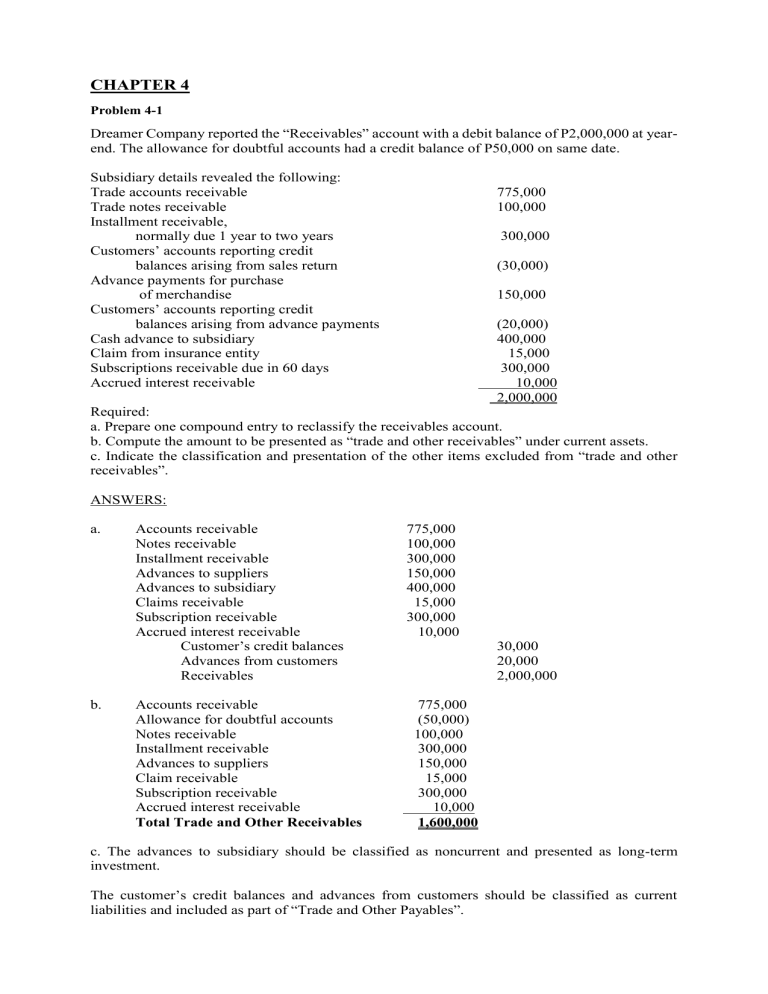

Okay, exactly what if during those times regarding boosting your credit, rates of interest increase step 1% and you will cost rise 10%? Your capability to cover a home try dramatically impacted, together with fee for similar residence is now as much as 23% high. The opportunity to get that house might just keeps slipped thanks to your fingertips. Big mistake!

That does not mean your credit history (a document that displays your credit score and you may score) are going to be an emergency (e

The fresh Virtual assistant Guarantee ‘s the lender’s exposure adjustor that enables them to get a threat on you. This new Va Guarantee out-of twenty-five% significantly decreases the lender’s chance of losses, in the same manner one to good 20%-25% down payment decreases the chance into antique financial. Essentially, the new Va Guarantee absorbs the danger that’s just like the brand new normal down payment. Advantage Experienced! You should never help make your borrowing from the bank blemishes an excuse so you’re able to postponed offered to buy a property. Once again, that might be a blunder.

Hopefully at this point you understand this we can improve statement, Credit scores aren’t one essential! He’s got just a marginal effect on this new costs open to Va financing applicants. As the Va program ‘s the lending marketplace’s borrowing exposure equalizer, they does away with necessity of superior borrowing that is required to possess antique money.

For those who have in the past calculated to hold faraway from seeking to buy a home because https://paydayloanalabama.com/rehobeth/ you think the credit ratings to have an excellent Va financing had a need to boost, then chances are you only haven’t securely evaluated your situation. There is certainly guarantee!

g., you cannot have a credit rating filled up with fees-offs, delinquencies and you can collection membership and you will expect you’ll getting recognized having an effective mortgage.) You need to work to keep the economic home managed. But if you had, such, a bankruptcy proceeding otherwise an existence knowledge such as for instance a disease, therefore resurrected oneself from all your crises and conserved the borrowing profile, youre more than likely nonetheless able to get an excellent Virtual assistant financing accepted.

(We shall secure the Wall structure Street gibberish to a minimum.) State anyone with a cards risk get away from 600 was provided a performance that will be as much as step 3/sixteen th higher than a borrower that has advanced borrowing from the bank otherwise a beneficial 740 get. Really, 3/16 th isn’t actually ? of 1%. (It’s simply a little more than step one/8 th .) And you may a person who got credit exposure results ranging from 620 and you may 660 might be offered a rate that’s step 1/8 th of just one% greater than someone who had superior borrowing chance scores of 720 or more. These all the way down borrowing from the bank chance get pages are getting considering decent cost, most likely.

Such as is the difference in financing offers to possess down credit scores, on involvement of Virtual assistant Guarantee. Got a credit risk rating from 600? That isn’t good get you could nonetheless get an excellent a good loan, by way of your own provider in addition to Va Guarantee. The latest Virtual assistant Warranty, facilitated by Virtual assistant Funding Commission, the cash one gets into the new Guarantee pond is the huge work with which makes everything work.

Mathematically, Virtual assistant fund default for a price higher that of its old-fashioned loan counterparts

The reason we was letting you know about the strengths (otherwise run out of thereof) out-of credit history is always to provide the you, the brand new Va buyer, a very over picture of what you’re against…and you can where you can catch some slack. People tends to be annoyed of the its credit score and genuinely believe that they must increase they prior to they’re able to pursue homeownership.

While you are carrying from trying to purchase property since do you believe your borrowing should increase, you’re shooting your self on the feet! Virtual assistant financing is likely currently around that have competitive cost. Those viewpoint your borrowing should be most readily useful be a little more applicable so you’re able to conventional underwriting to the traditional money.

{kind=link}